What In The World Is Happening: Common Sense & Digital Assets Can’t Seem to Find Alignment.

This week, I have an eclectic collection of stories for you. The theme, you might ask? Is common sense all that common?

Hello friends, strangers, acquaintances, and everything in between. I am back with another issue which, I’m sure, you’ve been eagerly awaiting.

Now, the digital asset world never ceases to amaze me. It moves at breakneck speed, and is as confusing as it is ingenious. Which is why, this week, I have an eclectic collection of stories for you. The theme, you might ask? Is common sense all that common?

Some highlights

What in the world is Proof of Stake (PoS)?

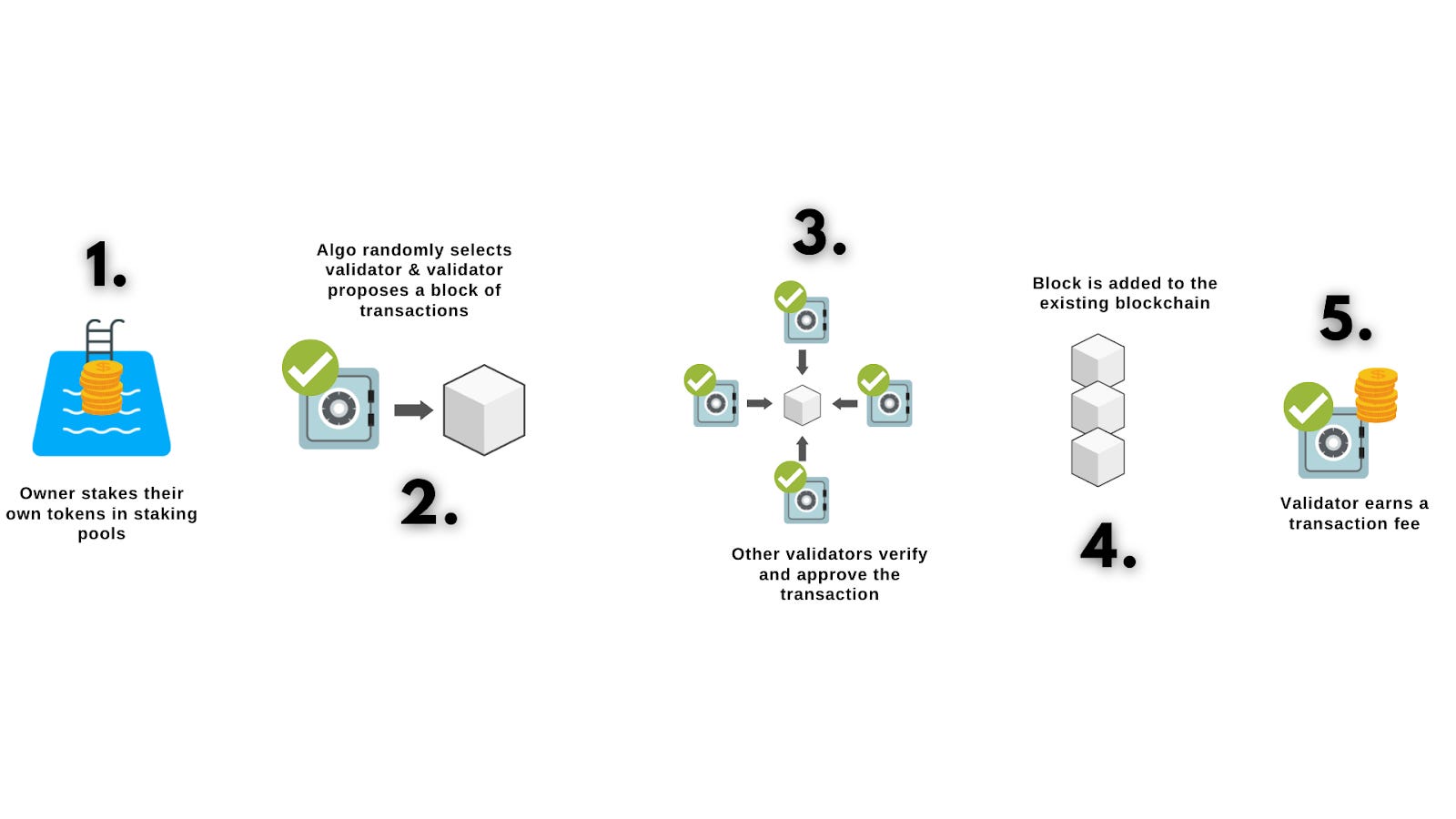

Readers, let’s start with the age old question:

“Where does the money come from?”

Now, for fiat, the answer is simple, it’s printed by the government (unless you ask your one “Facebook Auntie”, and she espouses the most egregious conspiracy theory in relation to money supply.) However, for digital tokens it is usually either proof of work or proof of stake. Today, we are going to attempt to untangle the proof of stake (PoS) model.

Both models rely on group action to create, verify, and guard the sequential record on the blockchain. Now, PoS requires the digital currency holder to validate block transactions, based on the amount of said currency a validator stakes.

In essence, PoS mechanisms just need validators to stake the currency in question. Now you might ask, how are validators assigned? Selection for the subsequent block writer (the validator) happens at random. There are higher odds assigned for those validators that have larger staked positions.

As much as I know you love reading, let me give you this handy little graphic:

Voyager wants to reward key staff…for going bankrupt?

Nothing says relatable and responsible like a company rewarding their staff members who so dutifully steered them to near disaster (or if you are an investor...just plain disaster.)

In a bizarre move, Voyager is attempting to pay employees a retention bonus and making zero effort to reduce headcount even after filing for bankruptcy. To date, they have roughly 350 employees on payroll. This key employee retention plan, “KERP”, as they have so creatively called it, is set to cost the company about $1.9M. This expenditure, according to the company, will “retain” thirty-eight “vital” employees due to their “valuable institutional knowledge”. These employees include some in accounting, cash and digital asset management, IT infrastructure, legal, and human resources (imagine paying everyone’s favorite HR person, Toby, a bonus).

The creditor committee, however, is adamant that this is a waste of money. You see, Voyager has zero evidence that these people plan to resign. In fact, only 12 employees have resigned since bankruptcy. The committee also pointed out that Voyager only has routine work to do now (the kind you get the first year intern to do I presume) and in the event of an uptick in work, they can always hire more people from the bevy of laid off people in the sector.

Crypto, Politics, and PACs: Seems like peak democracy to me

First off, to my pals that are not politically inclined (that includes you, fringe conspiracy enthusiast): What is a PAC?

PACs are political action committees, organized for the purpose of raising and spending money to elect and/or defeat candidates (sounds kind of like…a legalized bribe?). Most of these PACs represent some sort of interest (business, labor, ideology, etc.). We won’t dive into the legal specifics of what they can and can’t do, but I will say that PACs have pretty much been a wrecking ball on the sanctity of democracy. You get the gist.

Now, reader, lean in and listen: In recent congressional races in New York and Florida, crypto-linked PACs have poured about $3.6M on both sides of the aisle. This is primarily due to the fact that political figures in both states are quite outspoken about the digital asset industry. With DC lawmakers beginning to zero in on making regulations specific to the digital asset industry, this trend is expected to continue and (god-forbid) may lead to some crypto-focused Super PACs. These Super PACs can raise unlimited amounts of money but cannot contribute to the campaign, however, as there often are when it comes to politics, there are loopholes. It’s as shady as it sounds.

The question then, my friend, is do we as a collective society deem it acceptable to further allow the democratic process to be hijacked by sheer financial might? Do we permit our elected leaders to be beholden and swayed by forces outside of the public good? You tell me.

Celsius Update, “It’s not looking good bruv”

If you have been keeping up with my newsletter, which I know you have been, then you will be familiar with the meltdown of Celsius. Yes, that was a pun, and no, I am not sorry. If you’re not up to date, I am a bit disappointed. Read this newsletter!

No hard feelings though (hard feelings though, because I am a petty man), let me break it down quickly:

Crypto prices begin to fall at an astonishing rate.

Celsius froze client withdrawals, transfers, and swaps in mid June.

Celsius entered Chapter 11 bankruptcy last month (the lawyers had been pushing them for a while to do this.)

Debate began. Three big questions: who gets paid, when do they get paid and how much do they get paid?

To compound this situation, new court filings show that the company is running out of cash faster than a clueless tourist in a foreign open air market (be serious, why pay €100 for a fake Gucci bag in Istanbul). Some projections have them set to run out of funds by around October of 2022 (as of August, the company had a cash balance of $130M). Taking into consideration operating costs, capex, and restructuring costs, Celsius is set to be solely in the red by end of October as shown by the Monthly Cash Flow Table from law firm, Kirkland & Ellis:

This is made even worse by the fact that they still owe depositors about $2.8B more in digital currencies. Which, for the record, they don’t have. Big yikes.

The company has $348M in BTC on hand, yet has $2.5B in BTC liabilities. To make matters worse, there is about a $1B spread between ETH on hand and liabilities that are in the red. To make bad news even worse, there are even more shortfalls in other coins to compound the problem.

As if there weren’t enough bizarre twists to this saga, Celsius received approval to sell BTC that it has mined to cover operational expenses. This comes despite immense opposition to the Bitcoin Sale Motion from Shara Cornell, the US Trustee.

Cornell’s opposition seemed to be two fold; firstly the US Trustee pointed to documentation that hinted that, for the time being, this mining operation would be cash flow negative. As well, Cornell cited transparency concerns - her office has yet to receive succinct details over the associated costs and activities. These concerns were so strong, that she is considering appointing an examiner to the company to unravel this mess. A mess which is basically like 50lbs of necklaces and chains all twisted together…good luck untangling that.